The Anatomy of Loss

Last Friday, I gave a talk to a diverse group of professionals to explore a deceptively simple question in behavioral finance: Why is it so difficult to walk away from a losing position?

To illustrate this, I invited the audience to participate in a series of hypothetical coin-flip bets. In the first round, the stakes were symmetrical: Heads, you win $100; Tails, you lose $100. Despite it being a perfectly fair bet, very few hands went up.

I then increased the reward for winning to $150, and finally to $600, while keeping the potential loss at $100. It was only when the potential gain significantly outweighed the loss that the majority of the room felt comfortable participating.

This experiment demonstrates a powerful psychological phenomenon known as Loss Aversion.

Loss Aversion: When Pain Looms Larger Than Gain

The concept of loss aversion was introduced in 1979 by Daniel Kahneman and Amos Tversky in their foundational work on decision-making under uncertainty. Kahneman later received the Nobel Prize in Economics in 2002 for this research.

At its core, loss aversion suggests a simple but profound asymmetry: the pain of losing is psychologically more powerful than the pleasure of gaining. For most individuals, a $100 loss “stings” more than a $100 gain feels good. But recent research suggests the imbalance may be even more dramatic—especially when it comes to anticipation.

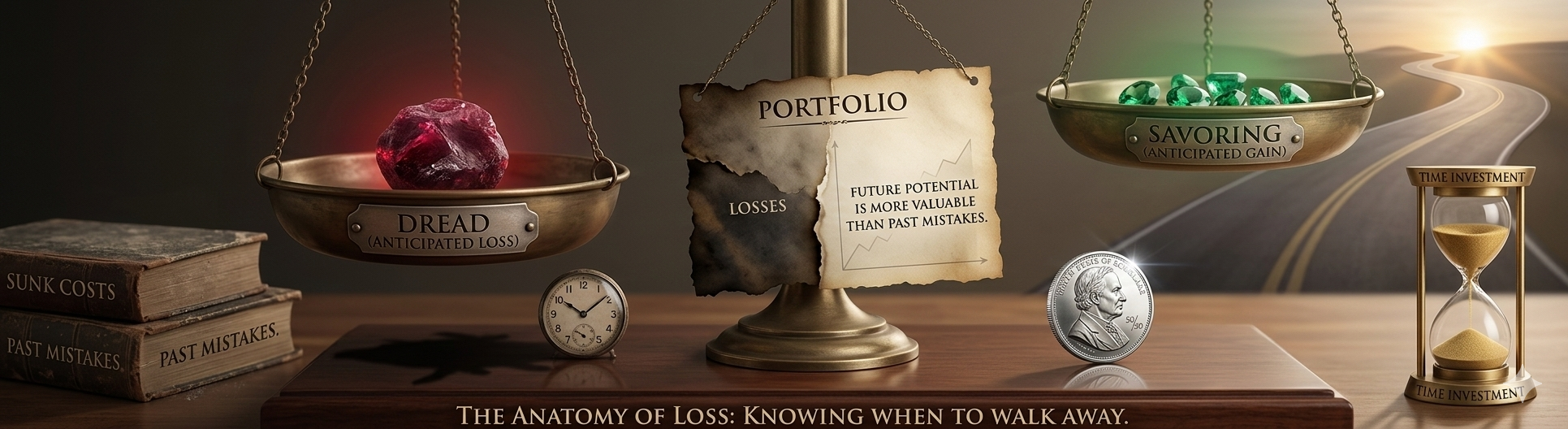

Dread vs. Savoring: The Emotional Multiplier

A long-term study titled Asymmetric Anticipatory Emotions and Economic Preferences analyzed nearly 14,000 individuals in the UK over three decades. The researchers examined how people emotionally respond not only to realized gains and losses, but to the anticipation of them. They identified two distinct emotional states:

Dread — the negative emotion experienced while anticipating a potential loss Savoring — the positive emotion experienced while anticipating a potential gain

The findings were striking.

The emotional intensity of anticipating a loss—dread—was estimated to be 6.19 times stronger than the pleasure of anticipating an equivalent gain—savoring.

This means our brains are disproportionately wired to avoid the emotional experience of potential loss, even before anything has happened. And that anticipatory imbalance often drives our decisions more than the actual outcomes.

The Realization Gap: When Reality Is Milder Than Fear

Interestingly, the research reveals a paradox. While the ratio between dread and savoring is 6.19, once gains and losses are actually realized, the asymmetry narrows significantly. When measuring emotional responses to realized outcomes, losses were found to be approximately 2.05 times more painful than equivalent gains were pleasurable.

In other words: we fear losses far more intensely than we ultimately experience them.Yet it is the anticipation—the dread—that keeps us stuck.

The “Disposition Effect” in Our Portfolios

In the world of finance, this instinct shapes our investment decisions in ways that often hurt our bottom line. It leads to a common behavior where investors sell their “winners” too quickly to lock in a sense of achievement, while holding onto “losers” far too long in hopes of a rebound.

I’ll be the first to admit I am not immune to this. I recently exited a losing position I held for nearly two years. At one point, it had declined by 60%. Rationally, I understood the thesis had weakened. But emotionally, selling would have forced me to crystallize the loss. Holding allowed me to defer the pain.

At the same time, I exited several winning positions early—seeking the immediate satisfaction of realized gains—only to watch them continue appreciating.

Dread kept me anchored to losers. Savoring pulled me out of winners.

The result was suboptimal capital allocation driven not by data, but by emotion.

Beyond the Markets: The Life Portfolio

Loss aversion extends far beyond financial assets. We apply this same logic to our “life portfolios” every day:

- We stay in a bad movie because we already paid for the ticket.

- We remain in unfulfilling careers because we invested years building expertise.

- We hold onto relationships long after they stop working because walking away would make the emotional loss explicit.

In finance, these are called sunk costs, irrecoverable investments that should not influence forward-looking decisions. Yet psychologically, they do. Holding on doesn’t recover time or capital; it simply adds an “opportunity cost”, the cost of not reallocating toward something better. Losses compound not just financially, but emotionally.

The Takeaway

The practical takeaway is not to eliminate emotion—that is neither realistic nor desirable. Rather, it is to recognize when anticipatory dread is distorting forward-looking judgment. Effective decision-making requires separating:

- Past investment

- Emotional discomfort

- Future expected value

Capital allocation, whether financial or personal, is ultimately a forward-looking exercise.Our past mistakes are informational; they are not obligations. The discipline to exit a losing position is not an admission of failure. It is an acknowledgment that future opportunity is more valuable than sunk emotional cost.

In investing, the ability to reallocate decisively is a competitive advantage. In life, it is a form of maturity. Understanding the anatomy of loss is not simply about minimizing downside, it is about optimizing future optionality.